Accretion/Dilution Analysis tries to answer an important question when it comes to corporate acquisitions – does the deal create or destroy value for shareholders of the buyer?

Answering this question requires analyzing what happens to Earnings Per Share (EPS) after the acquisition. The acquisition is accretive when the combined (Pro Forma) EPS are higher than the standalone forecast EPS of the buyer. It is dilutive when the Pro Forma EPS are lower than the standalone EPS.

To perform an Accretion/Dilution Analysis, you need to take the following steps:

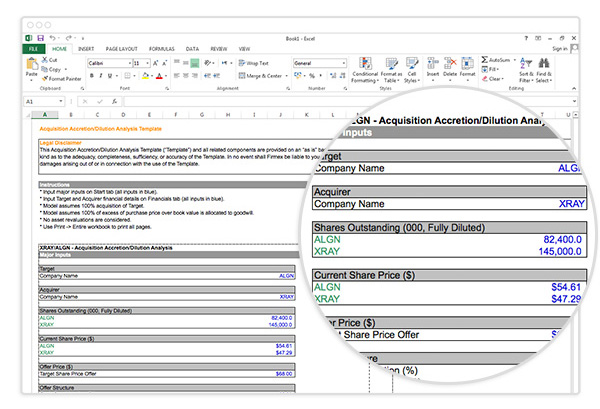

- Determine Acquisition Price: Price per share offered to target company shareholders multiplied by number of shares outstanding (fully diluted basis).

- Determine Offer Structure: Percentage of offer that will be paid in cash and percentage that will be paid in shares of the buyer, and any amount of additional debt the buyer needs to take on in order to have enough cash in aggregate.

- Calculate Post-Acquisition Shares Outstanding: If the buyer plans to finance all or part of the acquisition by issuing new shares, either through a share exchange or through a share issue to raise cash, these shares need to be added to the share count. If the acquisition is an all cash transaction the number of shares outstanding will not change.

- Estimate Synergies: Synergies that can be realized when combining the two businesses are an important aspect in the Accretion/Dilution Analysis, as they are a counterweight to the negative influence of an acquisition premium and transaction expenses. The amount of annual synergies after tax, whether from reduced overhead, manufacturing synergies, distribution efficiencies or other areas, should be estimated.

- Estimate Additional Interest Expense: The after-tax cost of any additional debt taken on by the buyer to finance the acquisition is calculated, as this is a new and incremental expense (note that this is only the cost of new debt added, not of total debt).

- Estimate Transaction Expenses: The after-tax transaction expenses are a negative influence on Pro-Forma Net Income in the period following the acquisition and should be estimated. Transaction expenses include advisory, share issuance, loan and due diligence fees.

- Estimate Pro-Forma Net Income: The forecast net income for the target company and the acquirer are added together with the estimated synergies. The additional interest expense and transaction expenses are then subtracted in order to arrive at Pro-Forma Net Income.

- Calculate Pro-Forma EPS: The Pro Forma Net Income of the combined business is divided by the Post-Acquisition Shares Outstanding to calculate Pro-Forma EPS.

- Accretion/Dilution Calculation: Pro-Forma EPS are divided by the standalone forecast EPS of the buyer and shown as a percentage. If the number is positive then the acquisition is accretive and positive for shareholders of the buyer; if it is negative the acquisition is dilutive and negative for shareholders. Subtracting the standalone forecast EPS of the buyer from the Pro-Forma EPS shows the accretion (positive) or dilution (negative) in dollar terms.

Before 2002, the amortization of goodwill was also an expense that needed to be considered and of course could have a significantly dilutive effect in some cases. However with the new accounting rules that did away with amortization if favor of impairment testing of goodwill we no longer need to do so.

In the past the Accretion/Dilution Analysis was mostly performed by just looking at the first year post-acquisition, but it is preferable to analyze a period of 3 to 5 years in order see the longer term impact of the transaction. This is especially so since many acquisitions are dilutive in the first year due to acquisition premiums paid and transaction expenses, but can become accretive thereafter if synergies are realized.

In the absence of synergies, an acquisition that is 100% paid for in shares will always be dilutive if the Price/Earnings (P/E) ratio of the target is higher than that of the buyer. Conversely an acquisition will be accretive if the P/E ration of the target is lower than that of the buyer. This fact has historically been a driver for much acquisition activity, with public companies buying privately held companies at lower multiples. Of course, this assumes that the P/E ratio of the combined entity will remain at the same level as that of the buyer which may not be the case and is a potential flaw with the Accretion/Dilution Analysis. After all, the target may very well deserve to have a lower P/E ratio and can bring down the P/E ratio of the buyer post-acquisition.

An acquisition that is accretive will generally be perceived as creating value for the shareholders of the buyer. Nevertheless not all dilutive transactions are bad, for example the acquisition of a company with higher earnings growth than the buyer may push up its P/E ratio and over time increase its earnings significantly even if it is dilutive short-term. In fact, a study performed by McKinsey & Company argues that the accretive or dilutive aspects of acquisitions have a limited impact on share prices.